You eat right, you work out regularly, you get plenty of sleep. You even get regular checkups from the doctor. Great! But how is your financial health?

If youre like most Americans, youre probably just a paycheck away from a financial crisis. In fact, according to Forbes, 60-percent of us dont have enough savings to cover a $500 emergency. Worse yet, 1 in 3 American families dont have ANY savings. At all. Scary.

So instead of asking whether or not youre financially fit, (why bother) were going to work on helping you rethink about how you view saving. How do you get your financial health as strong as your physical health? How do you get financially fit?

The fact is, financial fitness is just like any other workout plan it takes time, perseverance, and working SMART as well as working hard to meet your goals.

As you go through these steps, remember this. You dont get great legs by simply wishing away your thunder thighs. You dont get six pack abs by siting on the sofa. These financial fitness steps are WORK. And as the saying goes no pain, no gain.

So, get set to sweat ... here are your 7 Surefire Steps to Financial Fitness.

STEP 1 - Know Your Credit Score

Why is your credit score important? Do you want a new credit card? Do you need a loan to replace your gas guzzler? Then you NEED to know your credit score. Lending institutions use your score to decide if youll qualify for a loan or a credit card.

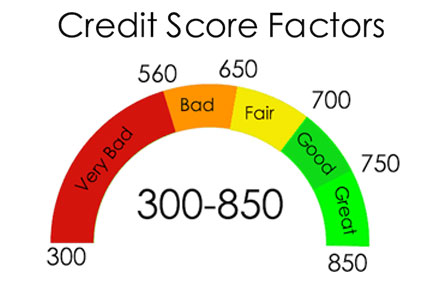

FICO credit scores range from 300 to 850. Any score above 680 is considered good.

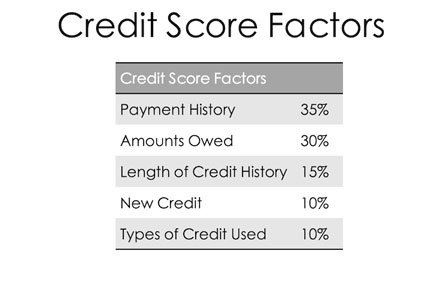

Your credit score is affected by several factors. Timely payment of any loans or credit cards increases your credit score -- late payments will hurt it.

STEP 2 Nail Your Debt-to-Cash Ratio

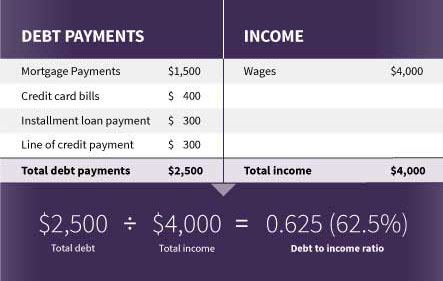

Your amount of debt relative to your disposable income affects your credit score. It may be stating the obvious, but you need to have more money coming in every month to cover debts and living expenses than is supposed to be going out.Your Debt-to-Income ratio (DTI) is an important factor in helping lenders decide whether or not youre a good risk.

In this technological age, lenders have access to a plethora of personal information on you. Thats why you need to keep your debt at a manageable level and make payments on time to maintain a good credit score. There are 3 reporting agencies where you can check your credit score for free -- Experian, Transunion and Equifax. They arent just looking at how well youve done at paying your bills, and paying them on time, they look at your amount of debt in relation to your finances.

If you have credit cards, theres no magic number you should have as a maximum or minimum, but the number of cards and their credit limits can affect your ability to get a loan.

What can hurt your ability to get a loan? If your amount owed on your credit cards and other revolving accounts is too high, that may put the loan you need for a major purchase out of reach.

Credit agencies suggest that building up to around 5 revolving accounts credit cards and loans over a period of time, is a good guideline to stay within. Just make sure you keep those balances low and pay on time.

If youre carrying too much debt, make a list of your revolving accounts, then make a plan to cut down that debt in a realistic but aggressive timeframe.

STEP 3 - Have Some Actual SAVINGS in the Bank

Do you have a savings account? The rule of thumb is you should have at least six months worth of expenses in savings so that if you lose your job, you have a cushion to rest on while getting back on your feet. Yes, it sounds painful but

remember that no pain saying from earlier?

STEP 4 -- Create a Monthly Budget and LIVE By It

Yes, that ugly six letter word

B U D G E T. If you dont have one that you follow monthly, you will NEVER become financially fit.

Creating a monthly budget is easy. Determine what the amount of your monthly take home pay. Add any investment income to that amount to come up with your Total Monthly Income, or TMI. Look at the number, smile, then prepare for the frown expenses.

Your monthly mortgage or rent, utilities, loan repayments, credit cards, groceries, gas (unless you drive an EV), and finally your fun stuff (shopping, dining out, etc.) make up your Monthly Expenses, or ME.

If your ME is more than your TMI, then your expenses are too much about

ME. (Its funny, but its true.) Now, if your TMI and ME are equal, guess what, its still too much about ME. Why? Youre missing that all-important third element Savings.

YConsider this -- you have an annual salary of $50,000 and monthly expenses of $3000, that means you should have $18,000 in savings at the ready. When more than half adults dont even have $2500 in the bank, thats a tall order.

Just as your body cant transform itself overnight, your savings cant magically appear. If your goal is $18,000 in savings, try to put aside $500 a month for 3 years. Think of it as a car payment and maybe take public transit for a while. Or cut up that credit card you just paid off and start paying yourself. Need some added incentive? Remember its easier to get a loan for a new car if youve got that kind of collateral in the bank.

Living within your budget is THE foundation of Financial Fitness. Bottom line, if youve got too much ME, either cut back expenses or get a promotion (or a new job) for a bigger TMI. And please remember, robbing a bank is NOT an option.

STEP 5 -- Contribute to Retirement Savings

Oh, you thought once youd stockpiled that six months of expenses youd be done with the whole savings thing. WRONG! Lets assume youre not going to go out and get run over by a bus, and will instead live a good, long, happy life and get to retire with your life partner and enjoy leisurely days for the remainder of your life. If you dont want your golden days to consist of living in a shelter or on the streets, youd better start saving.

What about your Social Security, you ask? The agency actually suggests that you expect it to cover only about 40% of your retirement expenses at most. Yes, even the government tells you to have an employer-based pension AND your own retirement savings to get by when youre at the age when everyone tells you how great you look yet no one will hire you.

Figuring out how much you need for retirement is a guessing game, but here are a few pointers to keep in mind.

- Most retirement experts suggest you expect your retirement income to be 70- to 80-percent of your pre-retirement earnings.

- Use the 4-percent rule to help determine your savings target for retirement income. If you need $60,000 to cover annual expenses, and you and your spouse get $3500 a month from Social Security, or $42,000 a year, you need to have $18,000 a year from a retirement savings fund. With savings of $450,000, 4-percent of that amount i.e. $18,000 -- will provide that additional income to meet those annual retirement expenses. FYI, the average monthly Social Security payment these days is $1666.00, not enough to cover rent in many places.

- According to a Fidelity Investments study, the average 65-year old couple will spend $260,000 in out-of-pocket expenses to cover medical costs throughout their retirement. Approximately 35-percent of retirees will spend some time in a long-term care facility, adding another $130,000 to overall medical expenses.

Bottom line if youre in your 20s or 30s, start saving NOW for retirement.

STEP 6 -- Own a Home? Plan for Maintenance Costs

So youve bought that starter home, or even better, your dream home. Now all your worries are over. Not quite. Now that youve got your home, you need to maintain it. And that costs money. And it probably requires savings. How much? There are a couple of rules you can use as a guide:

One rule is to save $1 per square foot of your home annually. If your home is 1500-square feet, you should save $1500 a year for maintenance. If your home is a new build, this may be the option you want to consider so youre not over-saving.

The standard approach is the 1-percent rule set aside 1% of the purchase price of your home each year for ongoing maintenance. This makes sense given the high cost of

well, everything right now, including home repair costs. So if your home cost $300,000, set aside $3,000 annually, or about $250 per month.

STEP 7 Tailor Your Insurance to Fit YOU

Last but not least, do you have insurance that covers your needs but doesnt cost you a fortune? Auto, home, health and life

these are the four corners of insurance that can either protect you and your family in times of trouble, or leave you high and dry at your most vulnerable moments.

Whether its health or auto insurance, your lifestyle is going to be a major factor in the type of insurance you need. Are you young, single and healthy? Your only major insurance need may be auto insurance (of course this doesnt apply if you take public transit or Uber everywhere).

If youre a homeowner in your 40s with a family, youll need to make sure you have adequate coverage on all fronts. And life insurance may be your most important consideration. In your 60s and an empty nester? Health insurance will likely be your highest priority.

Now you should be ready to start making some money moves that will get and keep you Financially Fit. Yes its hard work, but it is SO worth it!

END